Hey everyone! I’ve mostly started sharing my favorite memos and transcripts over at A Letter a Day, but as it’s more of a tasting menu, I’m reticent to post multiple memos or transcripts from the same person. That said, I’m thinking about booting this website back up as a place to share interesting things from people I’ve already featured on A Letter a Day.

This post is a transcript (and the slides) of Bill Gurley’s September 2023 talk “2,851 Miles.” I’ve already featured Bill in Letter #14, so I thought I’d share this here.

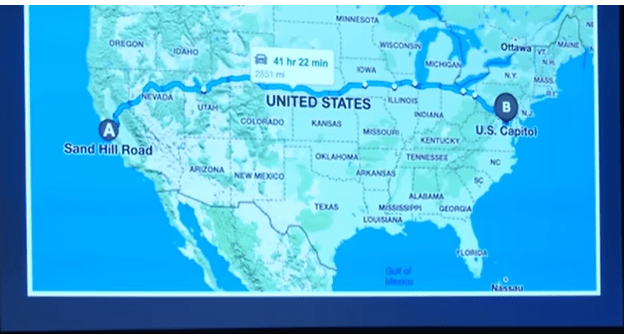

On Sept 12, 2023, Benchmark’s Bill Gurley gave a presentation at the All-In Summit titled “2,851 Miles” where he discussed the past, present, and future of regulatory capture in Silicon Valley.

He received a standing ovation and his presentation was dubbed “an instant classic.”

Former PayPal COO David Sacks immediately called it “the best talk in the history of All-In” and said “we need to get it out there immediately so it can start going viral. And I think it will go very viral.”

First Round’s Chris Fralic thought it was “So good. A Perfect TEDTalk” and “it’s gold.”

Shopify Founder and CEO Tobi Lutke commented that everyone should “definitely watch [Bill’s] incredible talk… once it comes out.”

One audience member liked it so much he yelled at Bill to run for President as the applause settled down.

I found the talk full of interesting anecdotes and wanted to be able to refer back to it easily, so I transcribed the talk and screengrabbed the slides. Sharing it below and also on Twitter (if you prefer threads).

Transcript

I’m Bill Gurley. I got to Silicon Valley in about 1997. And was fortunate enough to become a venture capitalist in 98. And the entire first year of my career, I had zero interest in interacting with any form of government. It didn’t seem necessary for what I was trying to do. I was working with founders and software and technology. I didn’t see what it would bring me.

Until one day where I ran into an issue, which I’ll tell you about later, that required me to understand what was going on in Washington. So I checked in with a few advisors, they introduced me to this lawyer in DC. Turns out, DC lawyers do a lot of things that aren’t lawyering. And he listened to what I had [to say], he said, I’ll call you back. He calls me back. He says, Bill, I got exactly what you need. I found a congressman on the committee that matters to what you’re talking about. And I can set up a meeting. I go Great, I’ll fly out. He goes, No, no, no, don’t fly out. He’s coming to you. He’s coming to me? That’s pretty nice. He goes, Do you have a conference room? I said, I’m a venture capitalist. We have lots of conference rooms. So he said, I need you to get some people together. And here’s the catch. They need to bring $5,000 each.

Hung up the phone. Started thinking, All right, I got six people. we got board member, CEO, $5000, $30,000. He calls me back next week — How’s it going? Great. I got six people, $5000 ready to go. He goes, Most of these meetings have 10 to 12 people. I said Shit. Like, now I’m inviting people that don’t even have anything to do with this thing and like having to help them out.

I’m up $60k. I hang up. He calls me back a week later. He goes, Bill, how’s it going? I go, Ah, shit. I got 12 people, everybody’s got a check, we’re ready to go. I’m losing interest at this point. He goes, Do they have spouses? I’m like, What kind of question is this, do they have spouses? He goes Yeah, let’s let’s have their spouses right $5,000 each. I go, Our conference room’s not big enough for the spouses! He goes, they don’t have to come.

This is a true story by the way, true story. And it would go on to happen two more times in my life and then I stopped meeting with congressmen.

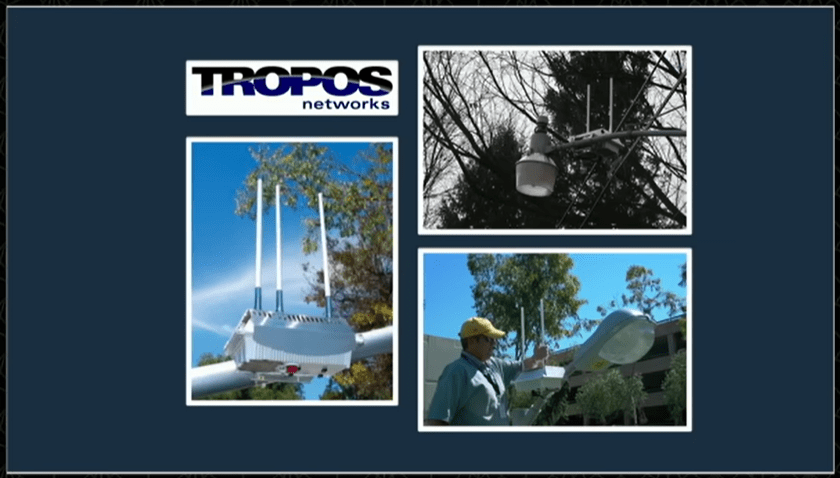

The reason that I needed to engage relates to this company. My fourth VC investment was in a company called Tropos Networks. We had an industrial grade mesh Wi-Fi, you could mount it on a telephone pole and bathe the city in Wi-Fi, broadband. It was awesome. We were so excited about it, we were changing the world. It was disruptive. Google got excited about it. Earthlink got excited about it. But the customer I loved the most that got excited about it where mayors. There were hundreds of mayors all over the country that wanted to provide free Wi-Fi service across their downtown area. It would help with public safety, economic development, and of course, digital divide. So, we were so thrilled, I was so pumped, I was sure we had a winner here.

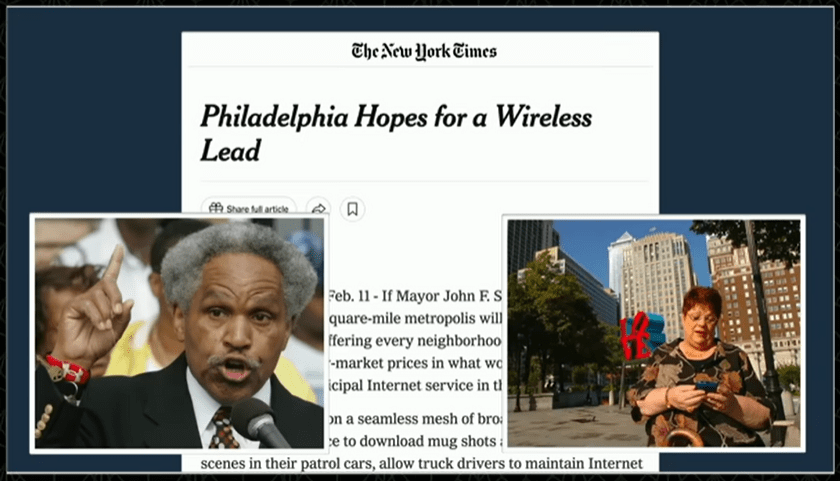

And then one day, these two people got excited, which turned out not to be a good thing. This is Mayor Street of Philadelphia and his CIO, Diana Neff. They got just as excited as I did. They were idealistic. They were optimistic. Maybe they were quixotic. Maybe I was too.

Because the next thing that happened is what caused me to get that meeting. You can’t read this, but it says Lobbyists Try to Kill Philly Wireless Plan. And in the article, it says Philly’s plan to offer an inexpensive wireless Internet service, the most ambitious yet, collided with commercial interests. Collided with commercial interests. There were no voters or citizens up in arms about this. Commercial interest.

How many of you–I know this is a younger crowd–how many of you are old enough to remember Schoolhouse Rock? Awesome. So like you, I learned about how Congress works by ABC Saturday morning television. And they told us–there’s a phrase in this–I looked up the script. It said some folks back home wanted a law, so they called their local congressman. Implying that the people that have the need are the citizens and the people that write the law, the congressmen.

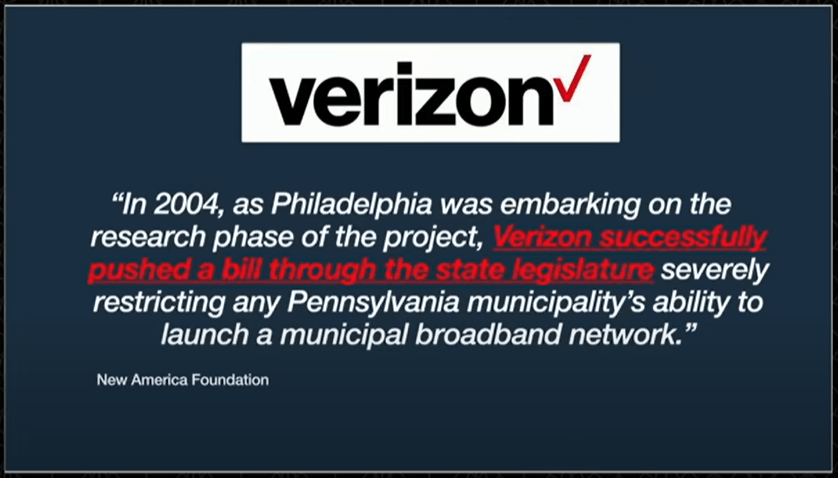

Imagine how surprised I was when I read this: Philadelphia was embarking on the research phase of the project when Verizon successfully pushed a bill through the state legislature. Verizon is writing legislation? How does that work? Now it turns out, this wasn’t even our biggest problem.

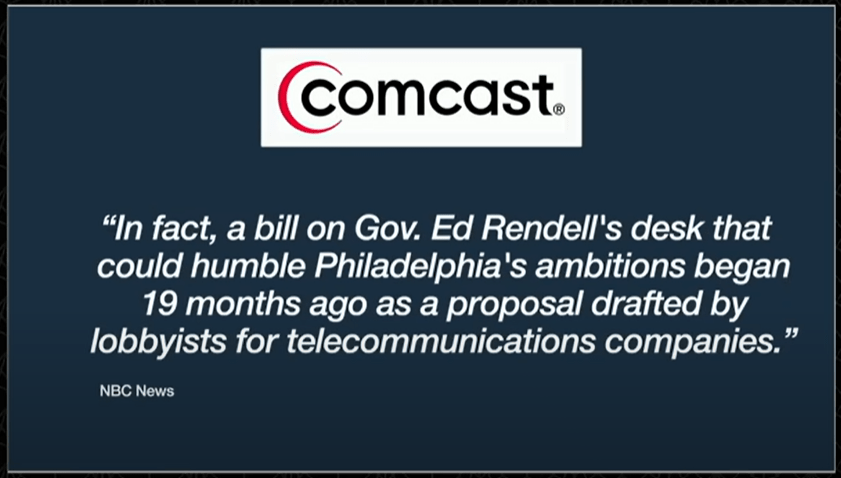

Because another company is headquartered in Philadelphia named Comcast. They had put a bill on Governor Rendell’s desk. Proposal drafted by lobbyists for the telecommunications companies. This isn’t what I learned on Schoolhouse Rock.

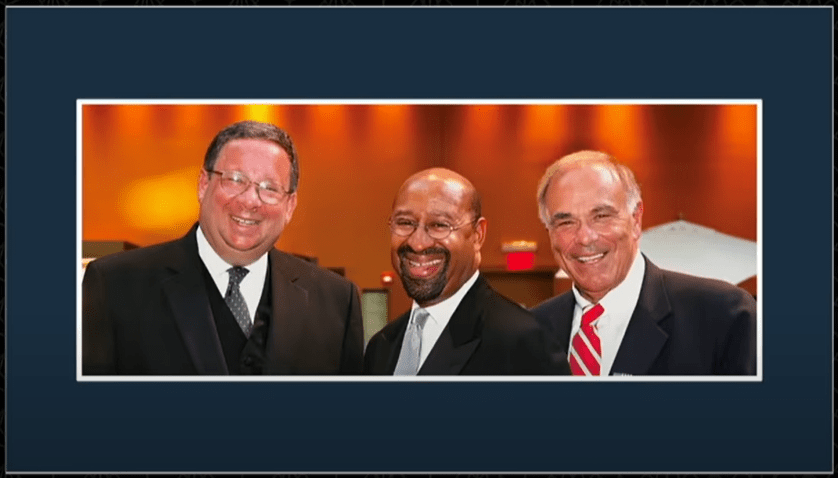

The governor whose bill that was on the desk of is Ed Rendell. He’s on the right. Before he was governor, he was mayor of Philadelphia. The gentleman in the middle is named Michael Nutter. He would go on to replace Street and was a longtime council member. But the guy on the left was the real nemesis. This is David Cohen, Chief Lobbyist for Comcast.

Now David Cohen is to corporate lobbying what Bob Marley is to reggae. He’s like, there’s just, there’s no second. The New York Times did a profile of him called Comcast’s Real Repairman, in which they say he is the most important executive in the whole company. And I fundamentally believe that. It also said he’s probably one of the most savvy corporate political operatives in the history of US business. The article on the right from The Enquirer calls him Philadelphia’s Most Powerful Unelected Official. I don’t even know how you can put those words together. So here we are. Here we are in our little conference room with our spousal-enhanced checkbooks. And this is like a second grader challenging Michael Jordan to a game of one on one for money. Like, we were pissing in the ocean. We had no chance. No chance.

Now, guess who offers citywide Wi Fi? That one’s easy.

AT&T would join this fight; within two years, they would outlaw municipal broadband in over 22 states. They’d just write it into the book. And just took the power of these local decision-makers away from them. All in the interest of the commercial interest, not the citizen.

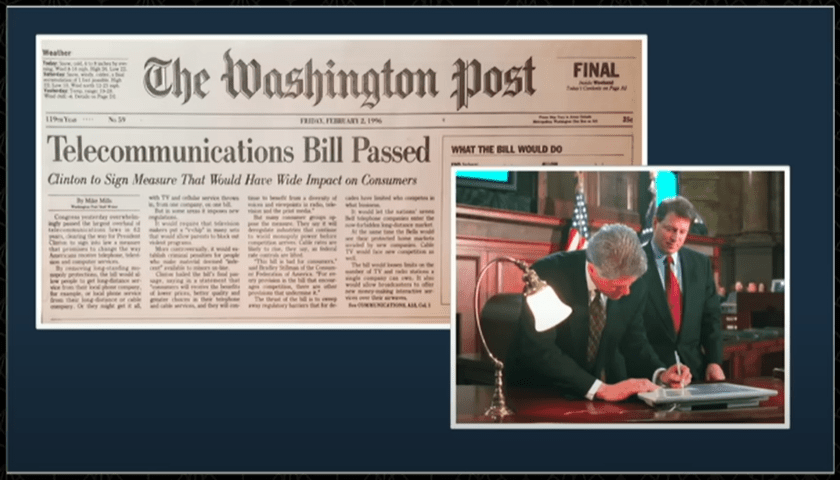

I want to talk about another piece of telecom legislation. My partnership back in those days invested in telecom equipment, and so we were very interested in the Telecommunications Act of 1996. This was heralded as the most important telecommunications reform in 62 years.

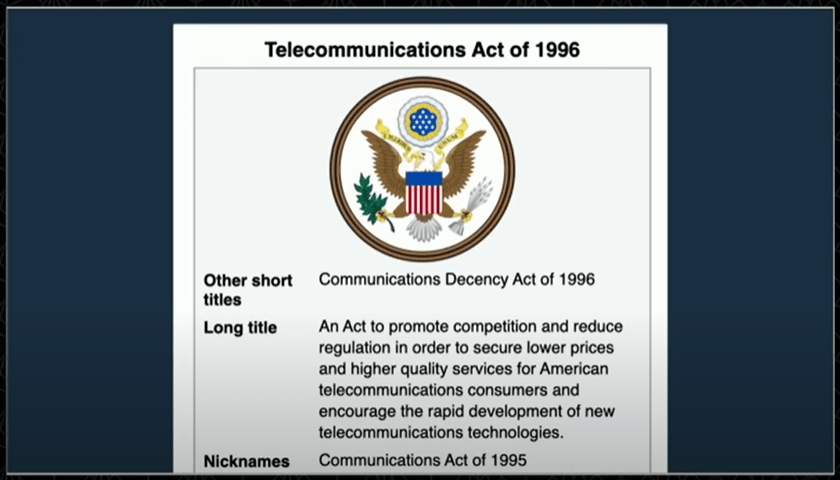

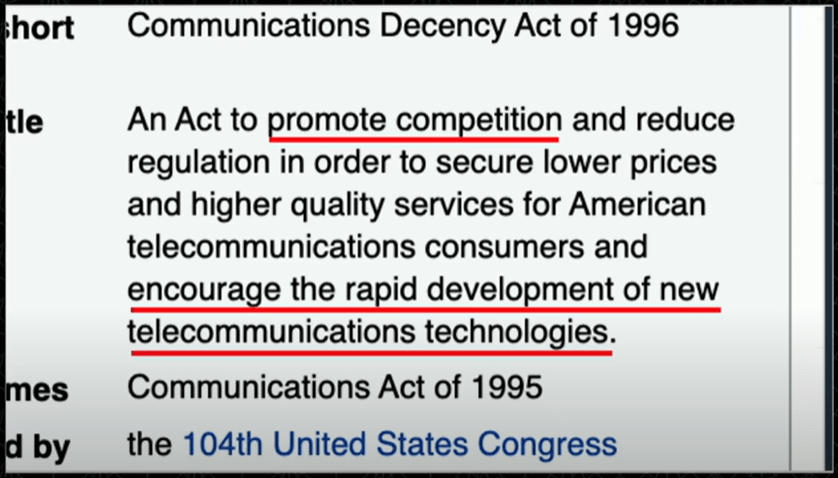

Now, this one’s simple. I’m just going to use the headlines from Wikipedia.

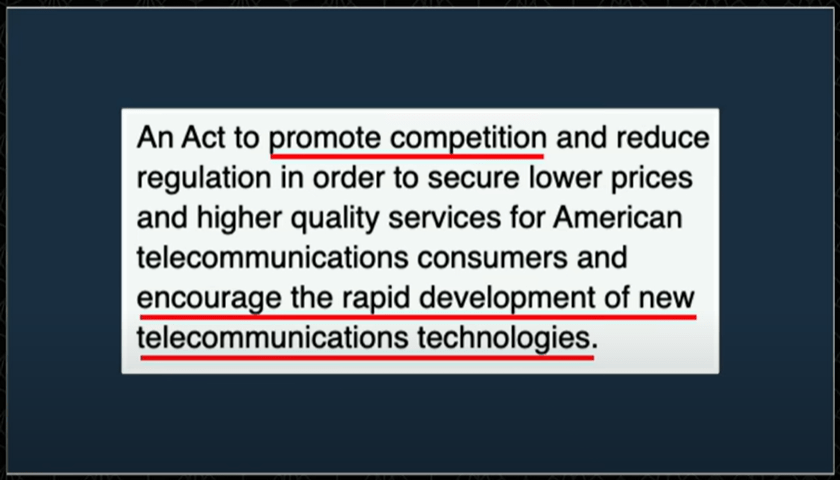

The Telecommunications Act of 1996 had two goals: to “promote competition,” and to “encourage the rapid development of new technologies.”

Let’s see how things went. In 1996, the top four had 48% market share. Four or five years later, after this heralded legislation, they’re up to 85%. That didn’t work.

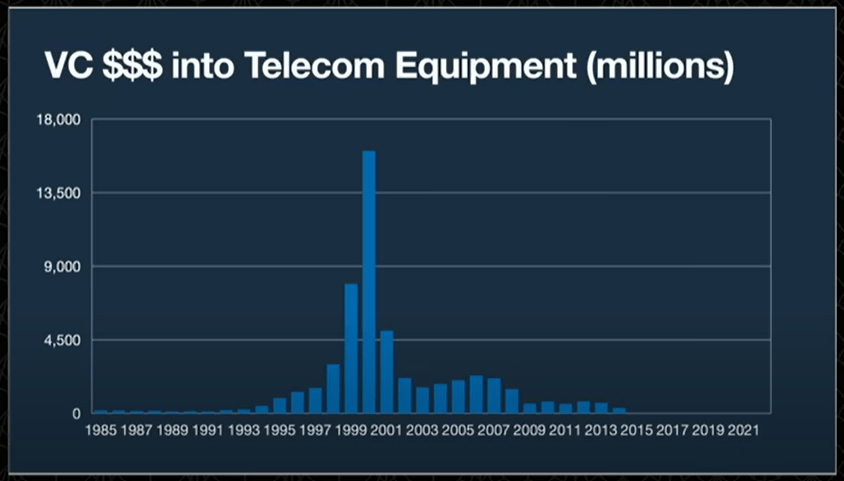

Let’s check in on the second one. Were they promoting innovation? This is a chart of VC dollars into telecom equipment. This used to be 15% of what VCs did. Within 10 years it had gone below 1%, and a year later, the NVCA stop tracking it. Now if you want to talk to one of the expert VCs in telecommunications equipment, it’ll be easy to do because they’re retired. This market’s gone. There is no more innovation in telecom equipment.

So what happens here? How can you possibly have a super important bill signed by, and implemented by, one of the most heralded presidents in our generation, that doesn’t just fail, failing would be things stay the same, and you don’t accomplish the goal. This did the did even worse. It created the opposite thing of what it was supposed to go do.

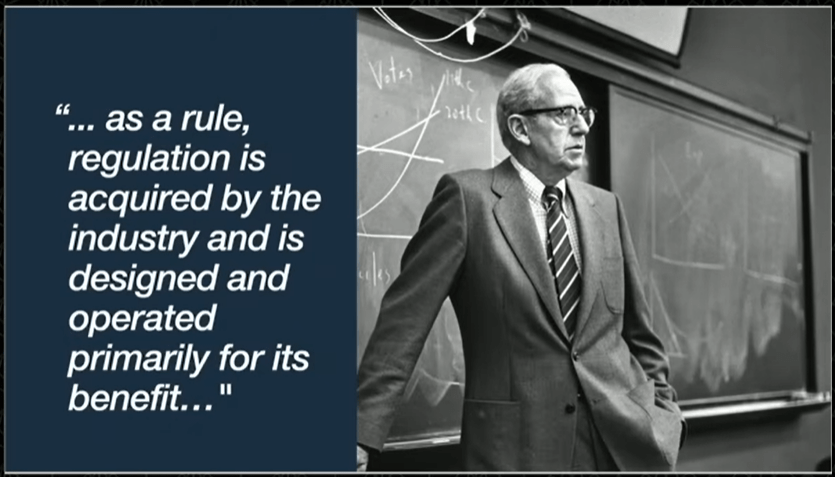

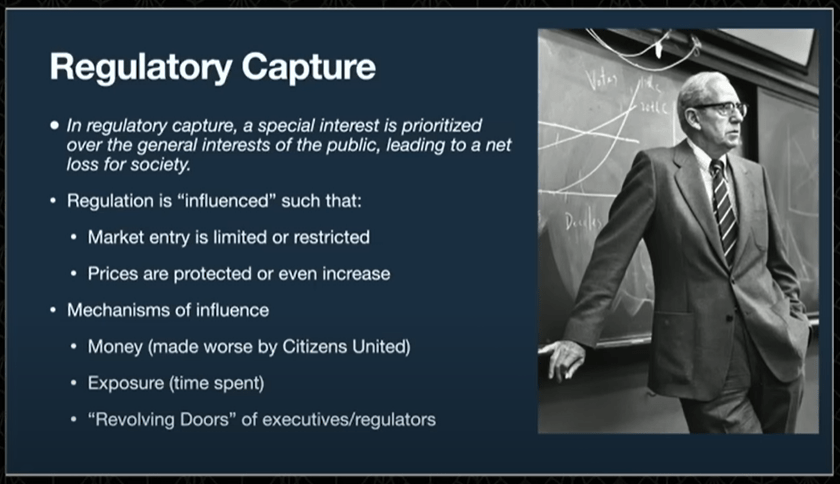

Let me introduce you to George Stigler. He’s the 1982 Nobel Prize winner in economics and the father of regulatory capture. This is his most famous quote: “As a rule, regulation is acquired by the industry and is designed and operated primarily for its benefit.” I like to say, “Regulation is the friend of the incumbent.” Quick audience interaction moment. That’s the one thing I want you to take away. So on the count of three, scream “regulation is the friend of the incumbent.” 1, 2, 3. [Audience shouts.] Yes! Amen! All right.

So, this is the only slide I have with bullets, because this is going to be a two minute Regulatory Capture 101. All from George Stigler’s notes. The first thing he says, “In regulatory capture, a special interest is prioritized over the general interests of the public,” — sound familiar from my other stories? — “leading to a net loss for society,” a net loss for society. That’s important. The two mechanisms they usually use is the second bullet, limited market entry and price protection, or even price increases, which I’ll show you more of. And then the mechanisms of influence are money, made worse by Citizens United, exposure, just time around people, and then three, revolving doors. This is super important, and I’ll show you one great example of that. That’s people moving in and out… When they interviewed Christie on the pod the other day, they were talking about this in the military.

All right, this is a piece of Morgan Stanley research from 1999. Someone took the time to go study five pieces of major US legislation that had happened over the years, and how the incumbent stocks did after the legislation. And let’s just steal a few sentences from this: “conclude that landmark regulatory action has a tendency to improve returns for the largest players in the targeted industry. Long term investors should consider capitalizing on any temporary weakness caused by market reaction to regulation. Many attempts to increase competition or improve customer experience have failed.” This is reinforcing what Stigler taught us.

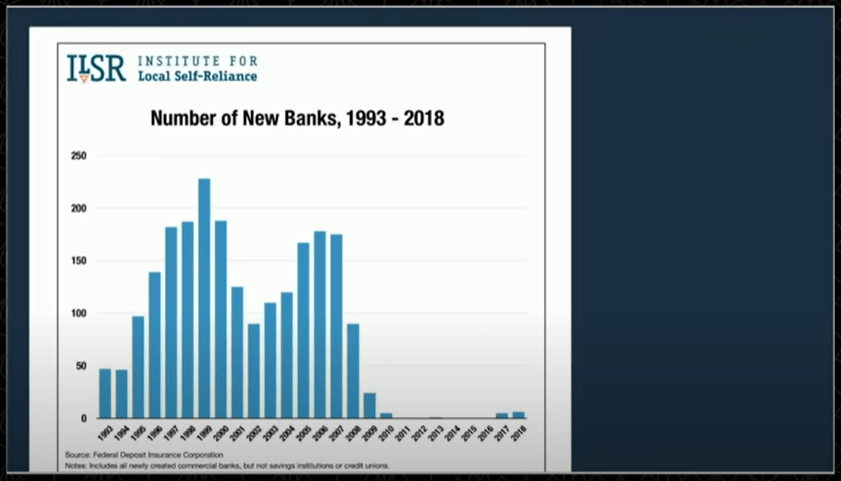

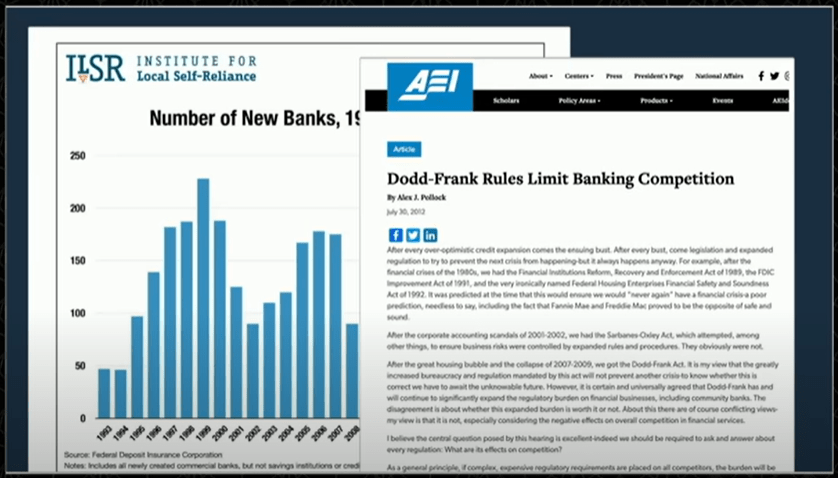

Here’s a very simple quick one. Number of new banks in the US. 2009, nothing.

Dodd Frank. Like, that’s what happens.

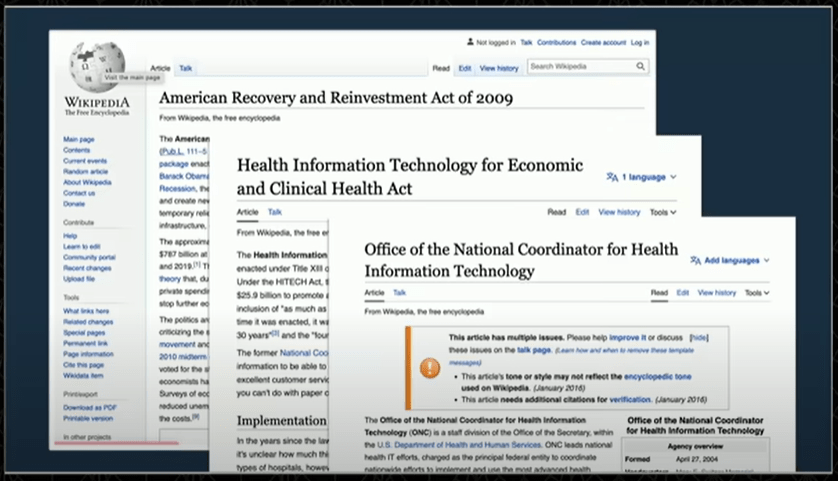

All right, two really good stories. You might not even believe them, because they’re so outlandish. Does everyone know who Epic is? It’s hard to know, because they’re not public. It’s a very large private company in Wisconsin that is the largest player in EHR software, medical records. And this is their CEO, Judith Faulkner. Now, in, get the year right, 2009, Obama put her on his Health IT Council. She was the only corporate representative. Should not surprise you that she’s a major donor to Obama.

Now, Obama passed the American Recovery Act, that was his big piece of stimulus, kind of like Biden’s inflation act that happened recently, and tucked underneath that, easy to hide in this big bill, is an act that was, the acronym’s HITECH, it’s this health information technology thing. And then they created an agency called ONC that oversaw it. Now, this is the part you’re not gonna believe. They came up with a brilliant idea. I have to assume she helped encourage this. Doctors would receive $44,000 each if they bought software. $38 billion. This is true, you can look it up. I’m not making it up. $44,000, give it to a doctor, implement some software. For many of you who run companies, that’d be pretty cool, right? The government passed a law, so they buy your software, they get money. It’d make it a lot easier.

Now, you may be thinking, Are doctors needy? But here’s the catch. You remember, this happened because of the mortgage meltdown. Doctors own multiple homes, so they have multiple mortgages, so they probably needed the assistance. Now, there’s two more things about this act that are also unbelievable. First, there’s a flaw. If someone said you’re gonna pay people to buy software, most people would be like, Well, you’re gonna have a problem. They’re gonna buy it and they’re not going to use it, right? Well, they thought of that. So guess what? The second phase, doctors got paid 17,000 more dollars to prove they were using it. It was called Meaningful Use. Plastered all over the website of all the EHR vendors at the time. It gets even better! So the the ONC decided the threshold of features you would need for your software to comply with this mandate. And I’m assuming they kind of took Epic’s feature set and plowed it into this spreadsheet. But they got the Department of Justice to enforce people that didn’t have the feature set that were getting the payments.

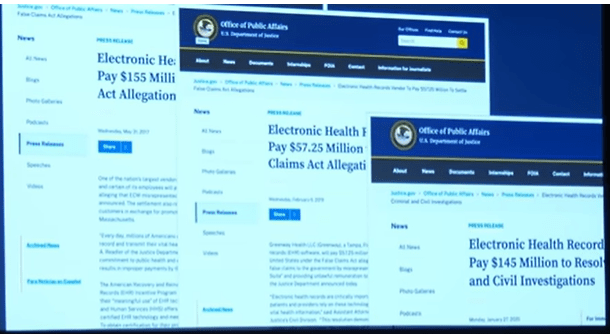

And you had three record fines. 155mn, 57mn, 145mn, against the lesser competitors of Epic. Unreal.

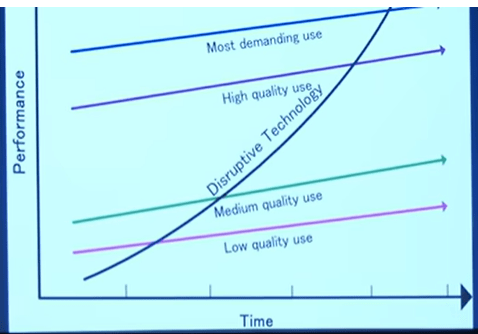

If you’ve studied the innovator’s dilemma, the way startups disrupt is they come in with lower feature products, but a feature that really matters to the customer in a simpler product, and they move up.

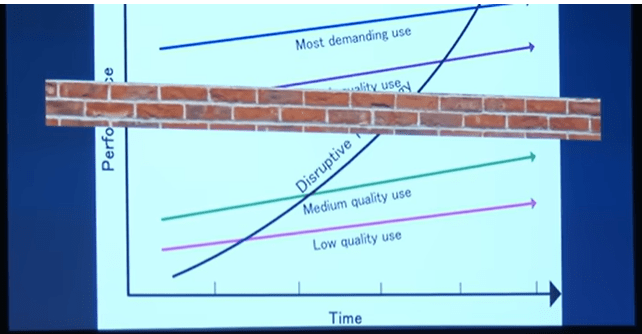

They put a brick wall there, so you couldn’t come up. It’s just amazing.

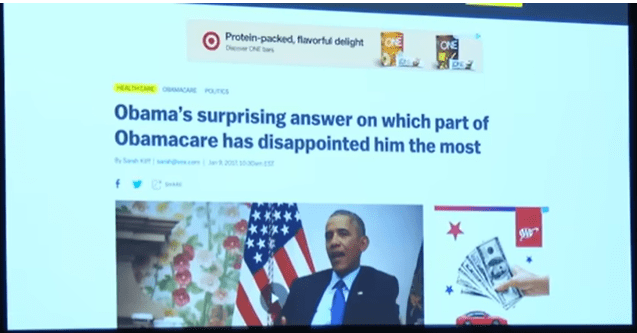

Obama, in an interview with Ezra Klein, said this was the most disappointing part of Obamacare. I mean, I think if any of us were in the room when they scratched this thing out, I could have told him it would have failed. I mean, paying people to do stuff is just… it’s not going to work.

Now you may ask, am I am I unhappy with Judith? I’m disgusted with it.

But, but, if I were a judge in the Olympic regulatory capture competition, I’m giving her a 10! This is fantastic. Fantastic!

All right, one more: revolving doors. This is one more.

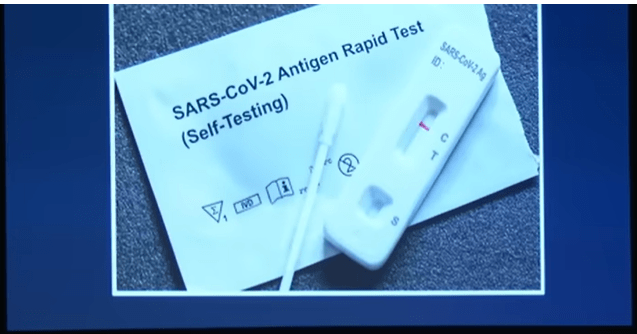

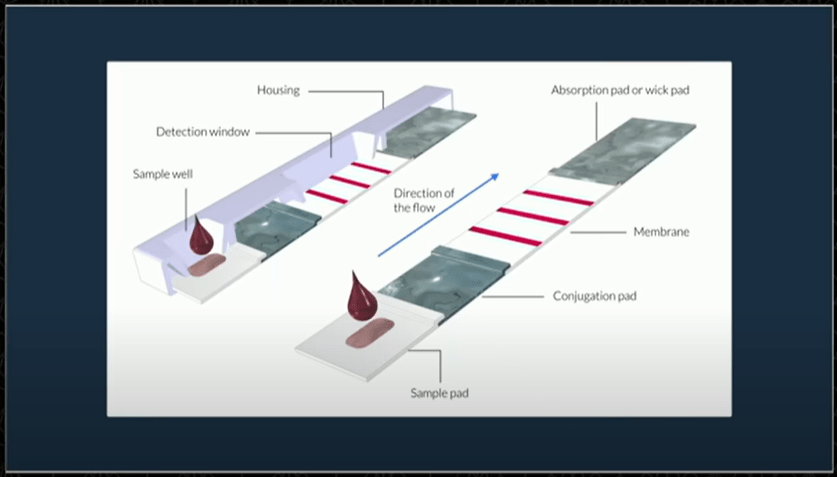

So, many of you know what this is. This is a COVID Rapid antigen test. Now, this is based on a very simple piece of technology — hopefully David will confirm this when it comes back up — called a lateral flow assay.

Now, this technology was developed 80 years ago in 1943, and it’s a complete commodity. The packaging almost doesn’t matter. You could probably use the strip without it. Now, before I tell you what happened in the US, let me tell you what happened in Europe.

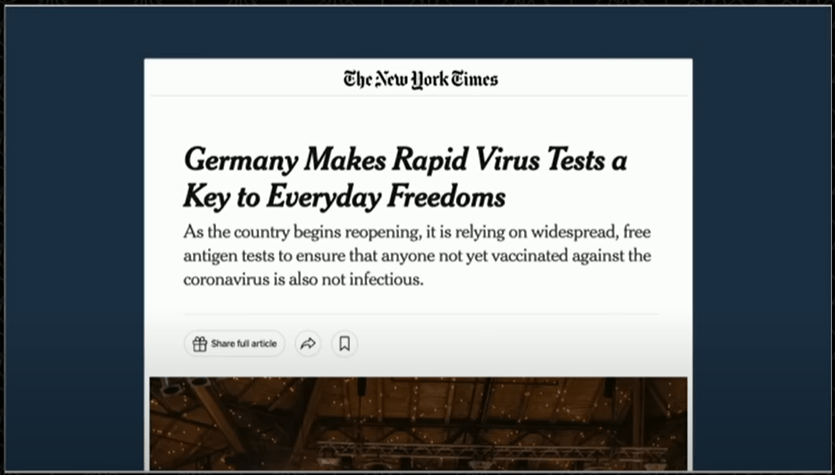

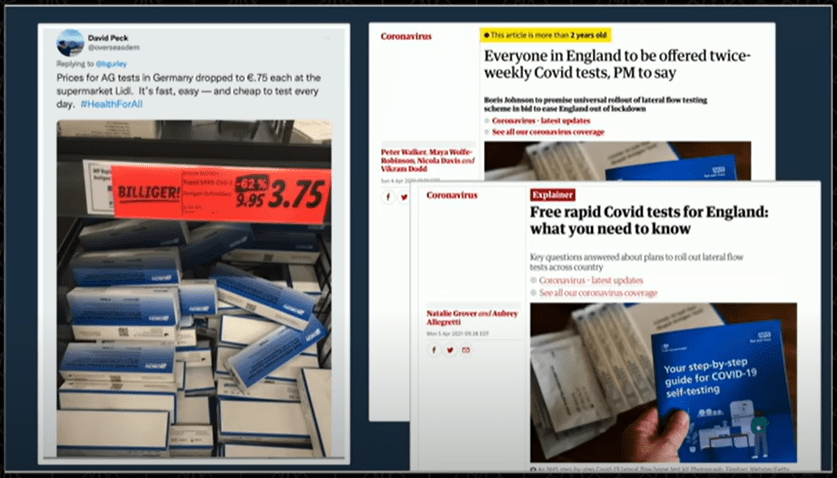

Germany leaned heavily into rapid tests. They got their scientists together, and they evaluated 122 different vendors, and validated 96 of them.

Here they are on the right, 96 different vendors that they okayed.

And as a result, in the German market, you could buy five tests for €3.75 or €0.75/test. UK leaned in as well. They got them in such numbers and so cheap they distributed them to people’s homes.

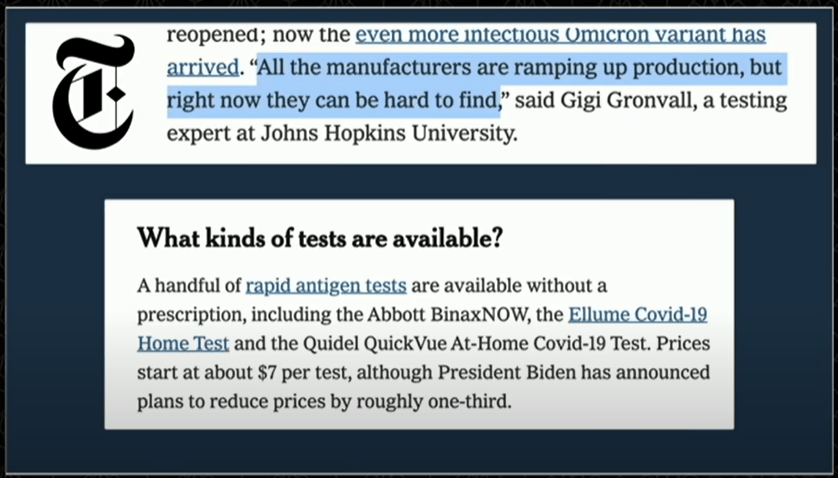

So what was going on in the US? Around that time, The New York Times did an article like, Here’s what’s going on with antigen tests. First of all, they fought them forever. And I think that may be capture as well, because the hospitals were making a ton of money on PCR tests. I think they they made as much money as they did on vaccines. But that’s another story. Here, it says all the manufacturers are ramping up production, but right now that they’re hard to find. And then it lists which tests are available, and they only list three vendors: Abbott, Ellume, and Quidel. Three vendors.

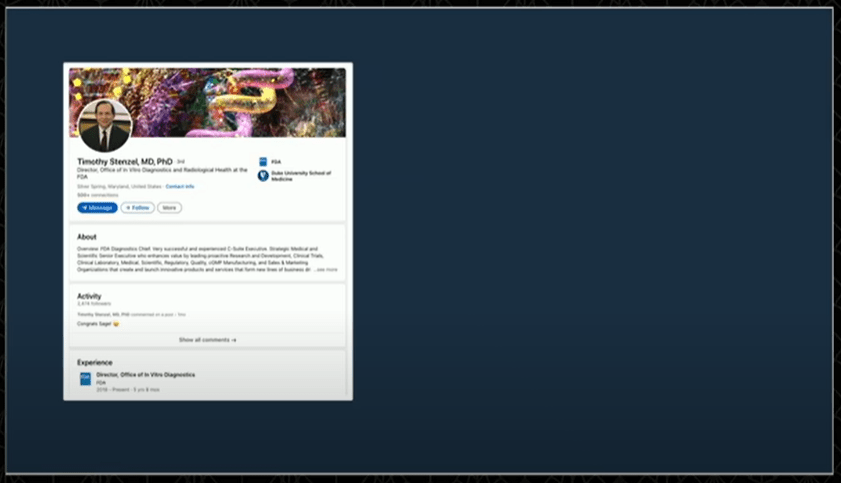

Now, you can play along on your phone. If you want to, go on LinkedIn. This guy’s name is Timothy Stenzel. Now, he works for the FDA. And he runs a group that oversees which antigen test gets approved. I know this because he would write scathing letters to the ones he rejected that you can also look up online.

Now, guess what? You’re not going to be surprised. Five years at Quidel. Four years at Abbott.

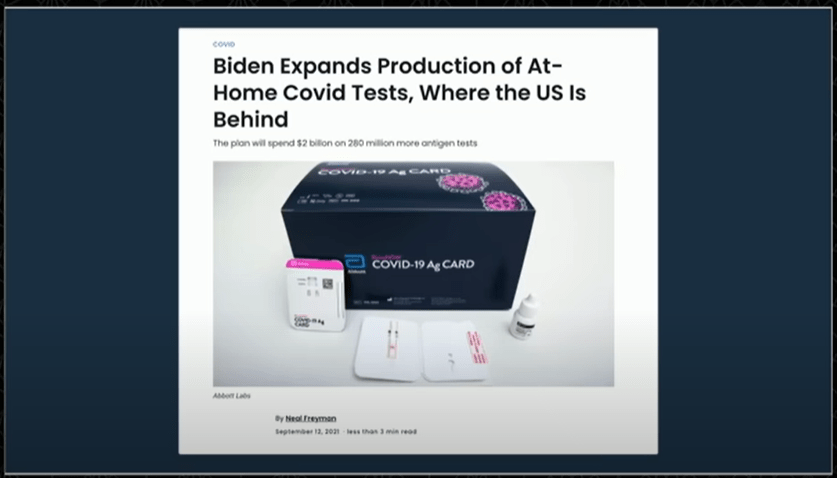

It gets worse. President Biden decided finally to lean into antigen tests and authorize $2 billion to go purchase tests. He should have gone to Germany and bought them out of the stores, but instead… but instead, he bought them from these guys. Now, I don’t know if you’ve ever used this test. All that packaging is complete and utter bullshit and unnecessary. That popsicle stick thing, like everyone else uses the lateral flow assay plastic thing that you can buy super cheap. This was over engineered.

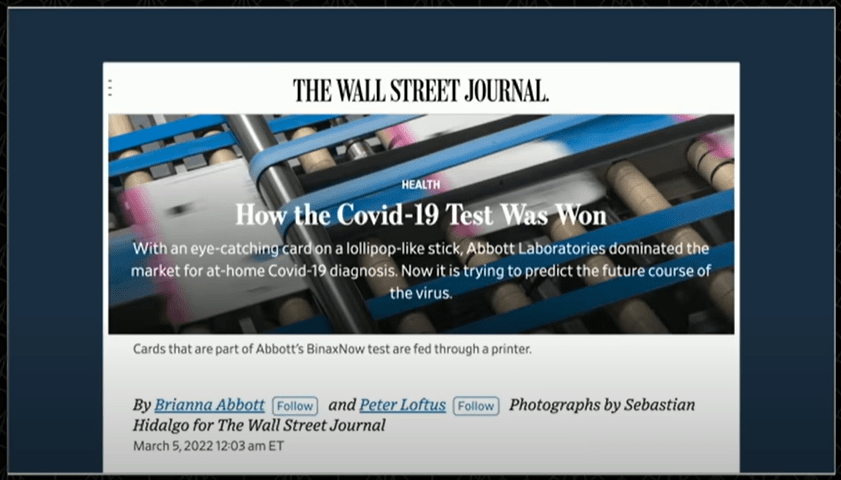

And then, and then I got really pissed. Because The Wall Street Journal wrote an article that was a victory lap for Abbott’s antigen test execution and how well they did in the market. And I’ve never met Brianna or Peter, but I hope they get to watch this because the first thing that should have done in the article is put a big picture of Timothy Stenzel, because that’s why this thing worked. And they write the eye-catching card on a lollipop stick as if though it was so cute, everyone bought it. Like, if you tried to sell that thing in Germany, how many would sell? Zero. Like, at $12 a test.

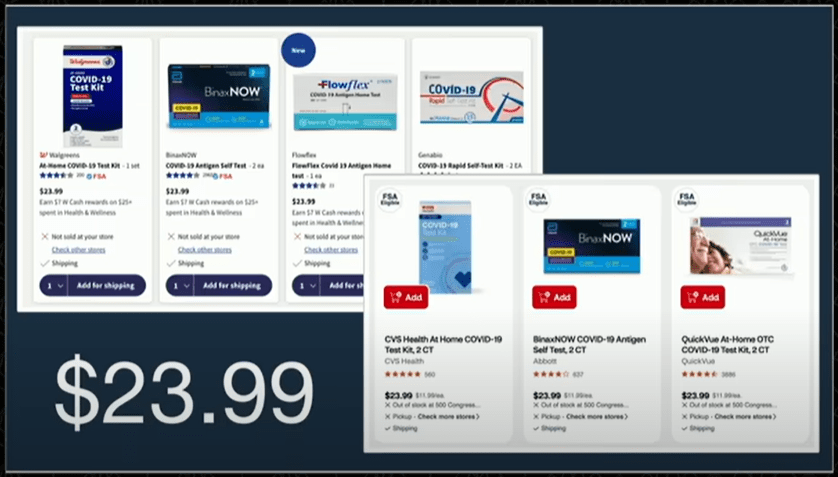

Yesterday, I — just for kicks, kinda, I went online. This is Walgreens and CVS antigen test. Their seven tests are all exactly $23.99. What is that? That’s not a marketplace. That’s not open competition. I also went on Boots, the famous UK — the tests are about $1.50, $1.60, per. Today! So you have a 6x differential in these tests today. And by the way, I’m not even talking about the fact that our citizenry may have been much enhanced by having rapid tests at a much lower price if they were treated as the commodity they were. Of course, they weren’t.

Now, Washington’s got its eyes on Silicon Valley. And it’s from both sides. We got Lindsey Graham, we got Elizabeth Warren.

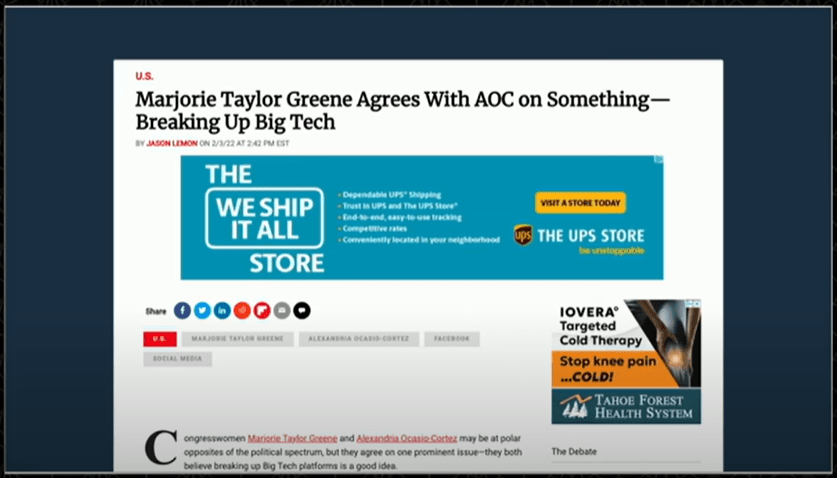

There’s an article here that says Marjorie Greene agrees with AOC — breaking up big tech. And you say why? Why are they so interested in tech?

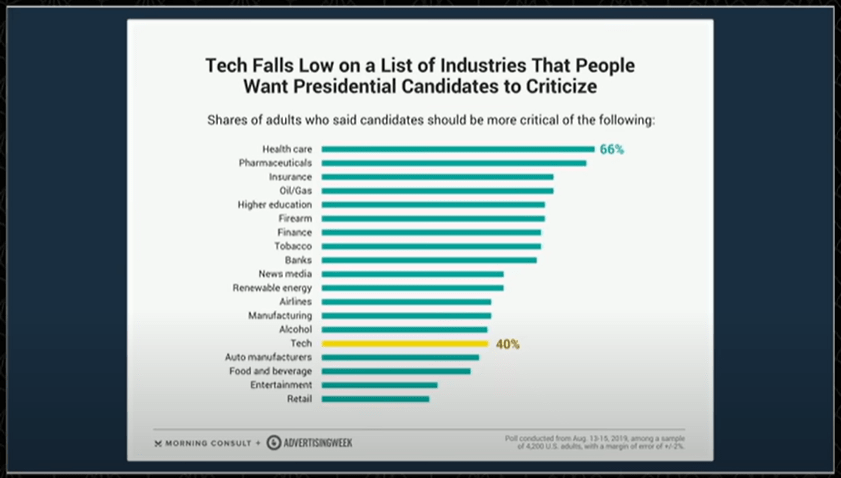

This is a poll of voters — voters don’t care. Voters are more worried about the industries where there’s a lot of regulatory capture. But they want to come after tech. I think I know why. I think they want them in the system, like the military, like finance, like telecom. They want them in the system because there’s money. Now, if Elizabeth Warren attacks big tech, you think they might go fund the competitor.

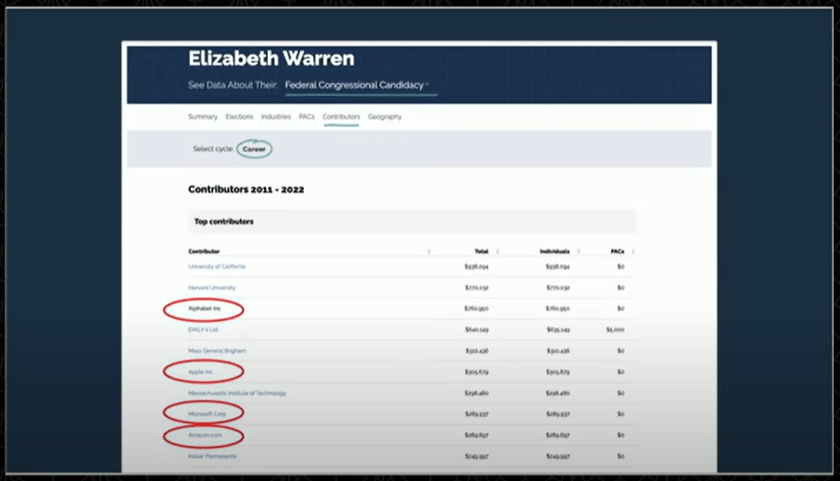

And you probably can’t read this, but this is OpenSecrets. Spend time on OpenSecrets. Four of the top 10 contributors to Elizabeth Warren are Alphabet, Apple, Microsoft, Amazon. You attack them, they have to come to you.

Some of our peers in Silicon Valley seem to want them to come too! I think they’ve read Stigler. Circle: please regulate us!

Brian’s on later, so this is risky: The more regulation — I think he’s right, by the way — the more regulation, the better for Coinbase. That’s exactly what Stigler would say.

Mark Zuckerberg needs, wants, and must have regulation. I get it, Mark!

And Sam’s just getting started. He wants regulation too!

Now, here’s a really scary thing in this AI space. The incumbents that are running to meet with all the government are spreading something that I don’t think is accurate or fair. They’re spreading a negative open source message. And I think it’s precisely because they know it’s their biggest threat. And I think what Meta’s done with Llama II is actually super interesting.

All right, I’m gonna wrap up with three things. Three takeaways. First, I’m not convinced we’re very good at regulation. All four of the stories I told you were failures. Like, they were a net loss for society, as Stigler says. This is a picture of Patrick Moynihan, who was one of the best senators I think we’ve ever had. He kept a picture of a pin behind his desk as a reminder. He felt like Congress should have to have something similar to the Hippocratic Oath that doctors have: First, do no harm. And the reason he has that point of view is he feels personally responsible for the homeless situation in America. He signed an act with JFK in 1963 that shut down the mental health institutions. It had a second piece that was supposed to prop something up. This happens with policy, second part didn’t happen, emptied out the mental health. And when everyone talks about the homeless problem, they should read this interview with him because they don’t go back and talk about this issue, but it’s very relevant. So I don’t think we’re very good at it. That’s the first thing.

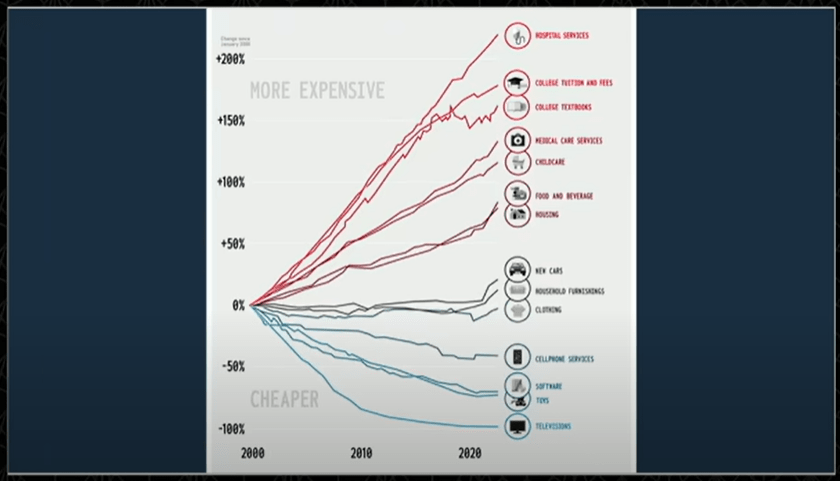

Second, I think regulatory capture gives capitalism a bad name. A couple people yesterday said, Oh, we got to fix capitalism. I think where capitalism is broken is where the capture’s the highest, right, like I just showed you some examples. You’ve seen these charts of price across time. And the highly competitive products coming out of Silicon Valley are dropping like crazy. It’s healthcare and education and those kinds of things where you have price increases.

Lastly, one of my favorite authors is Matt Ridley. And these two books really cover the span of human time. And he talks about how three things: technology, commerce, and the sharing of ideas, leads to prosperity for people, leads to increases in standard of living. And my big fear is that regulation is the opposite of this. It’s a blocker to innovation. So if you care about prosperity, and you kill innovation, you’re going to kill prosperity, from my point of view.

So, in closing, the reason I picked this title is Silicon Valley’s 2,851 miles away from Washington. And as these people put their eyes towards this, I would state the following: The reason Silicon Valley has been so successful is because it’s so fucking far away from Washington DC. Thank you.

Then, David Sacks, Jason Calacanis, Chamath Palihapitiya, and David Friedberg join Bill on stage for a discussion and Q&A. (Transcript to come.)

Wrap-up

If you’ve got any thoughts, questions, or feedback, please drop me a line – I would love to chat! You can find me on twitter at @kevg1412 or my email at kevin@12mv2.com.

If you’re a fan of business or technology in general, please check out some of my other projects!

- A Letter a Day — Memos, blog posts, transcripts (speeches, interviews, presentations), and more from investors like Todd Combs, Stan Druckenmiller, and John Doerr and Michael Moritz, founders like Steve Jobs, Sam Walton and Sergey Brin and Larry Page, and Operators like Peter Kaufman and Allen Zhang. More here.

- Speedwell Research — Comprehensive research on great public companies including Copart, Constellation Software, Floor & Decor, Meta, RH, interesting new frameworks like the Consumer’s Hierarchy of Preferences (Part 1, Part 2, Part 3), and much more.

- Cloud Valley — Easy to read, in-depth biographies that explore the defining moments, investments, and life decisions of investing, business, and tech legends like Dan Loeb, Bob Iger, Steve Jurvetson, and Cyan Banister.

- DJY Research — Comprehensive research on publicly-traded Asian companies like Alibaba, Tencent, Nintendo, Sea Limited (FREE SAMPLE), Coupang (FREE SAMPLE), and more.

- Compilations — “A national treasure — for every country.”

- Memos — A selection of some of my favorite investor memos.

- Bookshelves — Your favorite investors’/operators’ favorite books.